Here’s Why the Venture Capital Crash Will Hurt

by Michael Roth

The primary issue with the current valuation bubble is the industry’s inability to distribute returns to investors. LPs have continued to show faith in the venture capital industry, but their leniency may be what ends up hurting them whenever the bubble pops.

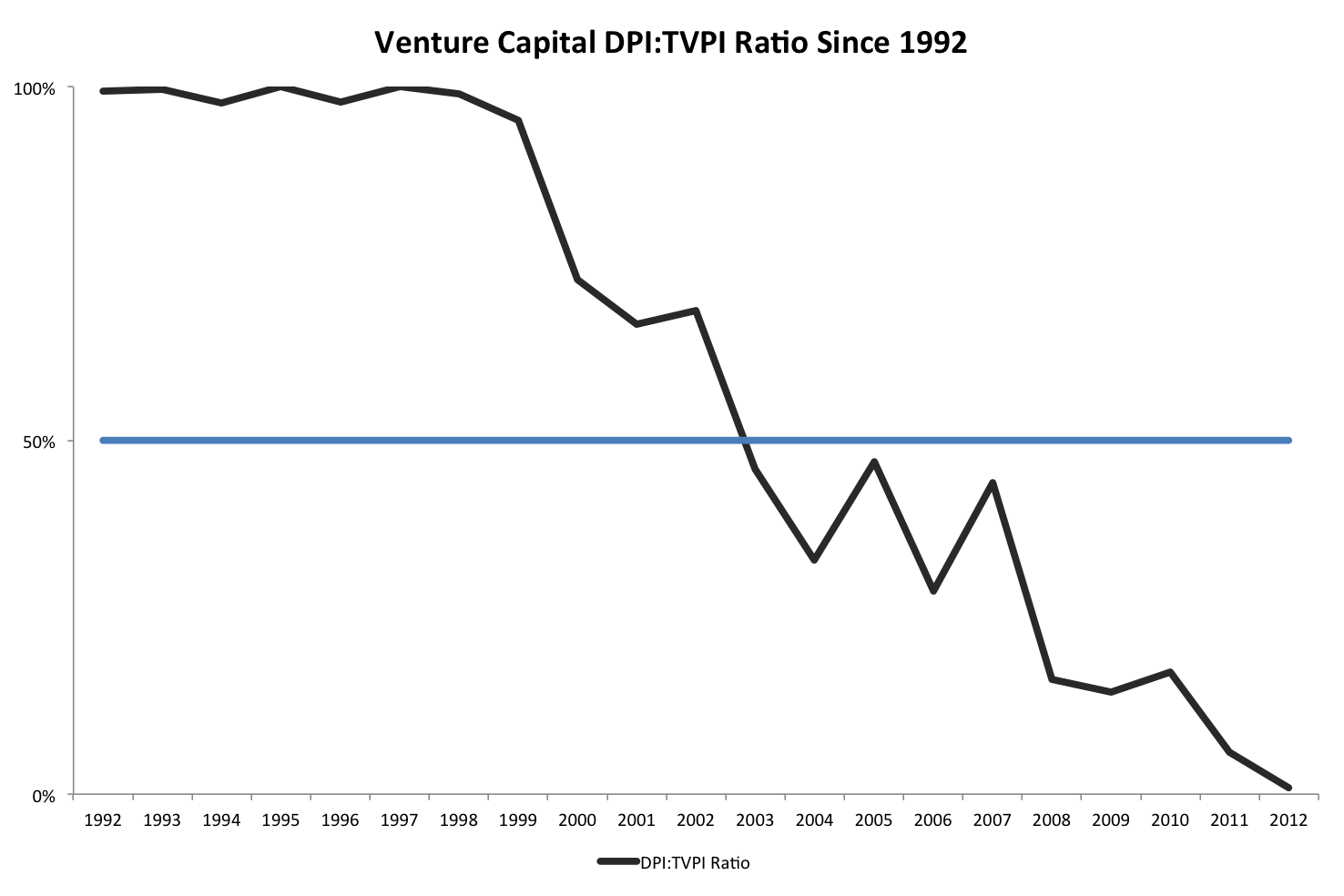

Half of the Industry’s Total Value Created Since 2003 Is Just “Paper Profits”

A good way to visualize the industry’s problem is too look at the ratio of DPI (distributed capital to paid in capital) to TVPI (total value to paid in capital). During a fund’s early years, you expect to see a large difference between between DPI and TVPI (ratio closer to 0%). As a fund gets closer to the end of its 10 year life, you expect the DPI and TVPI to converge. In the chart below, that is illustrated by the DPI:TVPI Ratio line approaching 100% as you move right to left.

Looking at the ratio can tell you one of two things:

- A lower ratio could be indicative of a portfolio that has good upside potential remaining.

- A lower ratio could be indicative of a portfolio that is having issues exiting portfolio companies and realizing returns.

The way to identify where a fund stands would be to compare it to its peers, but also to look at the age of the fund. As I mentioned, a fund approaching 10 years old should have a DPI:TVPI ratio that is approaching 100%.

Since 2003, the median DPI:TVPI ratio for the venture capital industry has been below 50%. This means that half of the total value created by the VC funds since 2003 is only on paper. Similarly, a large portion of the recent valuation increase for VC funds is only on paper and that is where it may stay unless VC firms begin to distribute returns.

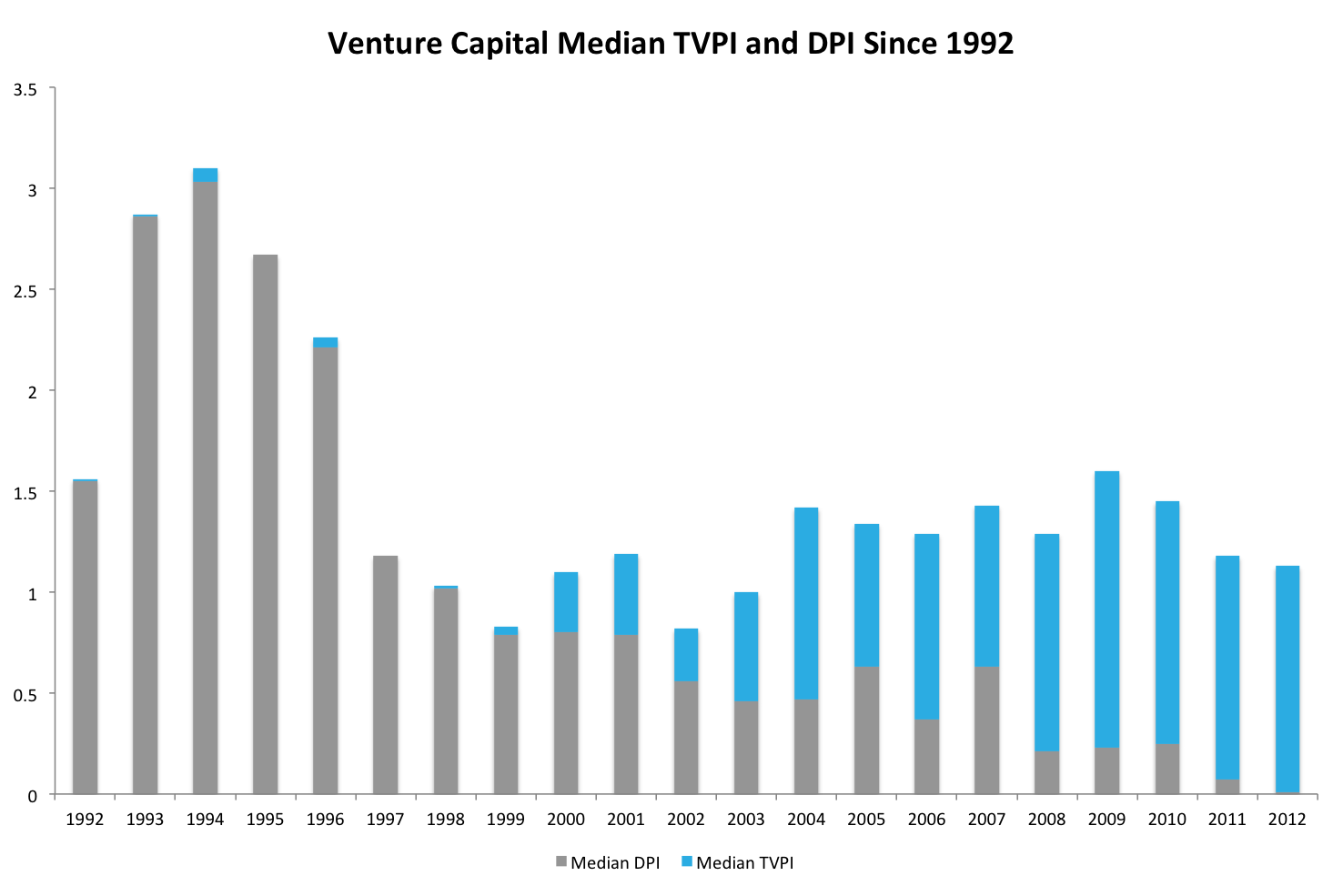

Half of the Funds Raised Since 1998 Have Distributed Less Than Investors Paid In

Another concern for the VC industry is the proportionate size of distributions. Specifically, looking at VC returns on an absolute basis, the industry has not had a strong DPI ratio since 1996, when distributions significantly exceeded paid in capital.

Worse yet, the median DPI ratio has not been greater than 1.0x since the 1998 vintage year. This means at least half of the funds raised since 1998 have yet to distribute a return in excess of paid in capital to investors since 1998. To give you a sense of how big of an issue this is, venture capital firms have raised $480 billion since 1999, according to NVCA figures.

By comparison, you only need to go back to 2003 to find a median DPI figure above 1.0x for the North American buyout industry.

What Does This Mean for the Current Euphoria?

The ability of managers to realize returns should be a real concern for investors in light of the recent rise in valuations. But looking at recent fundraising data, investors are buying into the hype. In 2014, venture capital firms raised more than $30 billion, which is well above the average amount raised since 2001. Investors seem to be putting a lot of faith in VC managers, their ability to value portfolio companies, and their ability to realize returns.

The amount of leeway given to venture firms is confounding since buyout firms are often advised by LPs to make some distributions from their existing portfolio before they consider going out fundraising again. LPs often say “show me some exits” before they feel comfortable recommitting to the next fund. With an average DPI:TVPI ratio of 16.5% for the 2007 – 2012 vintage years, venture capital firms may be avoiding this pressure for the most part. The average DPI: TVPI ratio for buyout funds of the same vintages is 22.5% (37% higher).

Wrapping Up

The VC industry’s inability to distribute returns to investors is a glaring deficiency that is leaving investors exposed to likelihood that valuations will come back down to earth. Unless there is a dramatic wave of distributions, the recent valuation bubble will be yet another painful lesson for LPs who seem to keep forgetting the industry’s inability to distribute returns.

Don’t worry about the VCs though. They will still be earning a 2% fee on the record amount of capital they have recently raised.